Economic sentiment indicator

04. Jul 2025

Construction confidence is fading

The Economic Sentiment Indicator (ESI) provides a snapshot of economic optimism by combining survey responses from consumers (households) and businesses. Consumers contribute 20% to the overall index. The remaining 80% comes from four key industrial sectors, each weighted according to their economic contribution: primary sector (40%), services (30%), retail (5%) and construction (5%).

[px-graph-1]

The ESI currently stands at 8, which is below the long-term average of 14. The table below shows confidence trends from each six-monthly survey.

[px-graph-2]

Households less optimistic about economy’s one-year outlook

Faroese households are less optimistic about the economy than they have been in the past two years, with the consumer confidence indicator currently standing at -17. Households are less optimistic about both the overall economic outlook and their private finances in the year ahead compared to today.

[px-graph-3]

More than a quarter struggle to make ends meet

Some 27% of the surveyed households say they only just manage to make ends meet. Three years ago, this figure was 20%. About 56% of households are saving small amounts, while 6% report saving substantial amounts. Despite significant consumer price hikes in recent years, borrowing does not appear to have increased. 9% report using their savings.

[px-graph-4]

Will consumer spending increase?

Consumer patterns affect the retail sector, as Faroese households purchase a large portion of the goods offered by this sector. More consumers are reporting that now is the right time for major purchases such as furniture and electronic items. Meanwhile, fewer consumers plan to spend substantial amounts on home improvements, compared to the previous survey.

[px-graph-5]

Consumers rarely believe there is an ideal time to buy a car, though this general sentiment is trending downward slightly.

Survey questions and graphs are available on the consumer page.

Declining confidence for retailers

Retail sector optimism has fallen slightly, with the retail trade confidence indicator dropping from 13 to 10. Consumer price growth is slower than it has been in the past three years. While retailers anticipate slower sales in the coming year, they expect an increased demand for staff in the next 12 months, though not as much as half a year ago.

[px-graph-6]

Survey questions and graphs are available on the retail trade page.

Construction confidence fading

Construction confidence fell from 17 to -1, well below the long-term average of 22. The construction sector's vulnerability to the economic cycle is evident in the major fluctuations seen in the graph below.

[px-graph-7]

Construction firms have seen a decrease in orders and project a decline in staff demand over the next 12 months.

[px-graph-8]

Staff shortage was the most significant factor limiting production in the construction sector, cited by 47% of firms. Low demand was a constraint for 24%, while 16% cited poor weather.

Survey questions and graphs are available on the construction page.

Less pessimism in primary sector and industries

The industrial confidence indicator remains unchanged at -3, below the long-term average of 9. Firms in the primary sector and industry are expecting a slight decrease in production in the year ahead. The firms also expect lower selling prices.

[px-graph-9]

The Faroese primary sector is affected by global economic cycles as it is heavily reliant on exports. There has been a notable increase in orders from abroad, and firms report an improvement in international market share.

Service optimism on the rise

Increased optimism is evident in the service sector, where surveyed companies reported satisfactory turnover. This trend is expected to continue, with an anticipated increase in turnover over the next year.

[px-graph-10]

Survey questions and graphs are available on the primary-sectors page and services page.

About the tendency survey

The economic tendency survey consists of indicators that measure economic optimism among consumers and businesses. The major element of this survey is the economic sentiment indicator (ESI), a composite indicator compiled twice a year (January and June) that calculates the confidence that consumers and the main four industrial sectors have in the economy.

Rather than reflecting a direct measure of economic activity, the ESI, a weighted index from five questionnaires, represents the difference between the percentages of respondents giving positive and negative replies about their current and projected economic outlook.

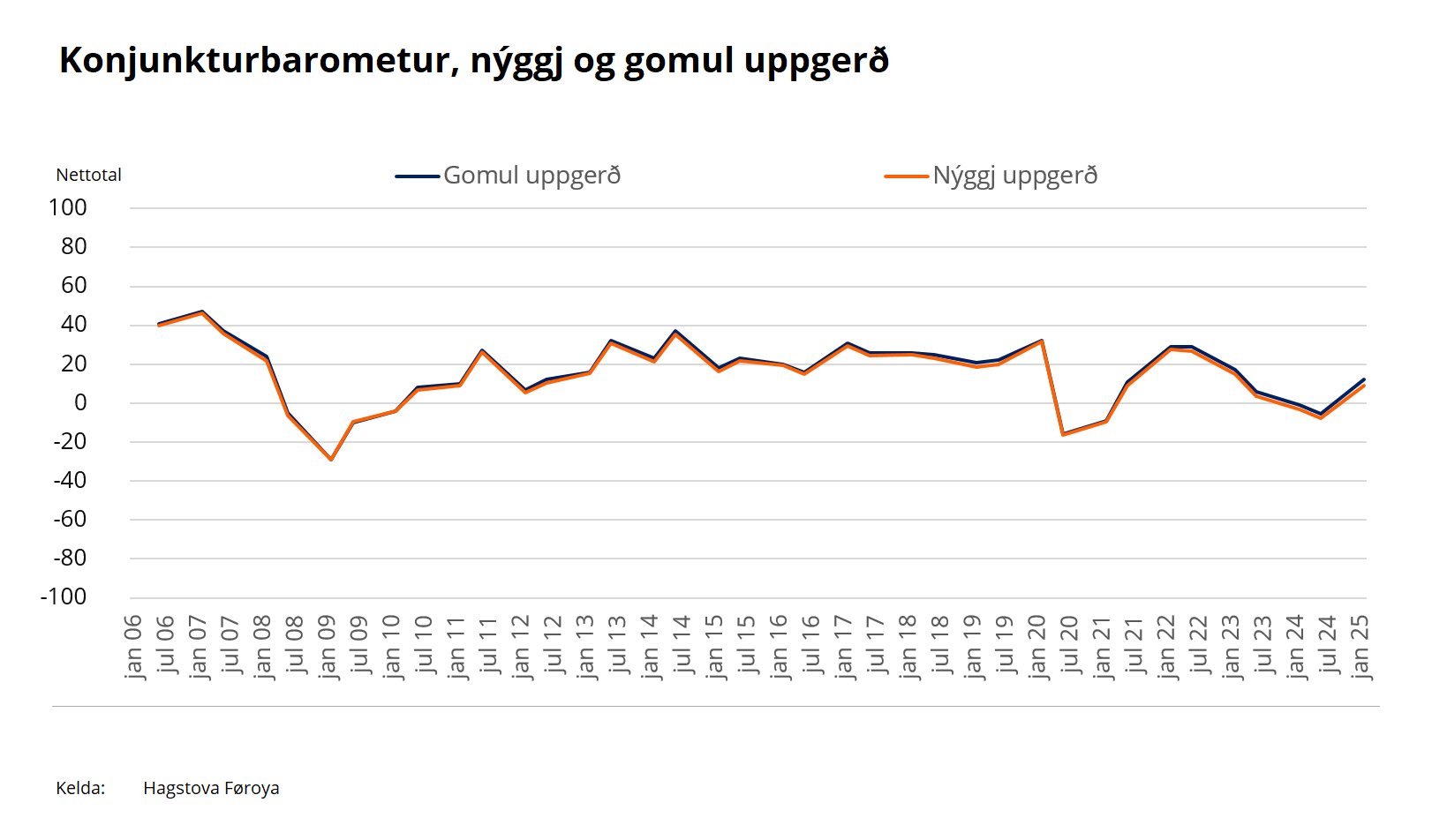

Revised survey methodology

Following updated guidance on business cycle barometers in 2024, this latest ESI report incorporates revised survey questions and methodologies, now aligned with those used in all ECFIN member states. These revisions facilitate international comparisons.

The index for the consumer survey is calculated as the average of the net scores in the following four questions:

- How has your household's financial situation changed over the past 12 months?

- How do you expect your household's financial situation to change in the next 12 months?

- How do you think the Faroese economy will fare over the next 12 months?

- Do you expect your household to make more major purchases (such as furniture or electronic items) in the next 12 months than in the previous 12 months?

The graph below shows how methodological revisions affect the data retrospectively.